Market Overview:

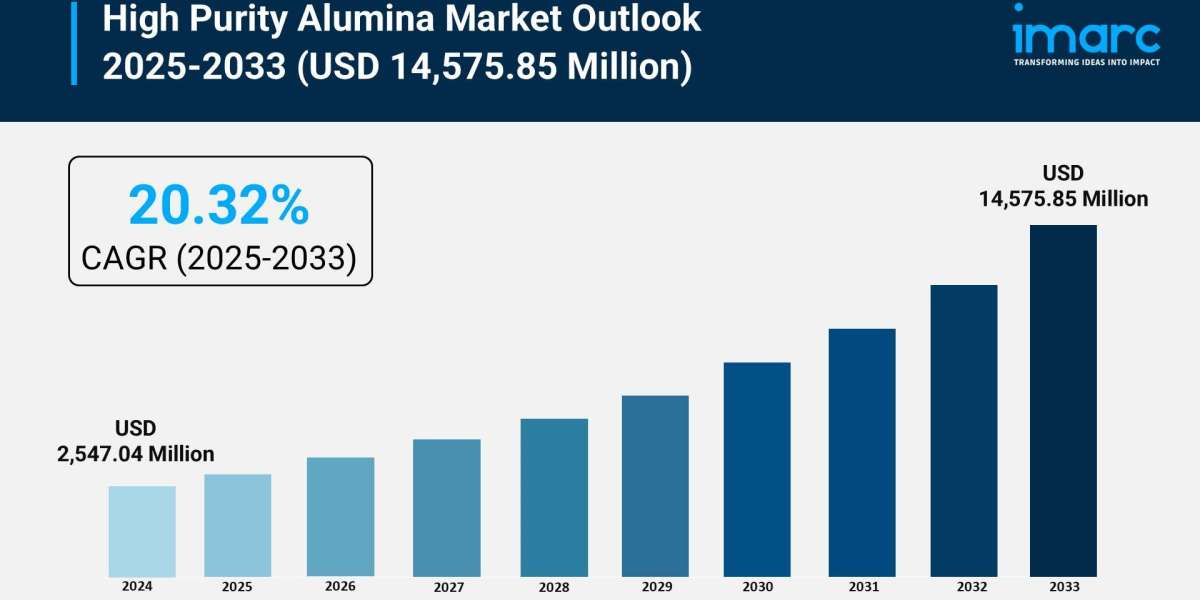

The high purity alumina market is experiencing rapid growth, driven by surging demand from the electric vehicle (ev) and energy storage sector, global adoption of energy-efficient led lighting, and expansion of the advanced electronics and semiconductor industry. According to IMARC Group’s latest research publication, “High Purity Alumina Market Size, Share, Trends and Forecast by Purity Level, Production Method, Application, and Region, 2025-2033”, The global high purity alumina market size was valued at USD 2,547.04 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 14,575.85 Million by 2033, exhibiting a CAGR of 20.32% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/high-purity-alumina-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the High Purity Alumina Market

- Surging Demand from the Electric Vehicle (EV) and Energy Storage Sector

The shift towards electrification of transportation and the increasing need for large-scale renewable energy storage are major catalysts for HPA demand. HPA is a vital material used as a protective coating on separators within lithium-ion (Li-ion) batteries, which are the power source for EVs and energy storage systems. This coating enhances the battery's thermal stability and safety by preventing shrinkage and reducing the risk of thermal runaway, a critical performance factor for high-capacity batteries. Currently, the global production of electric cars is in the tens of millions, and over 22 million EV battery packs have required ceramic-coated separators, with a significant majority utilizing HPA. This necessity for superior safety and performance in Li-ion batteries, supported by global government initiatives promoting zero-emission vehicles, creates a massive, sustained pull for high-purity materials in the battery manufacturing value chain. The energy storage end-use segment is projected to be the fastest-growing application area for HPA.

- Global Adoption of Energy-Efficient LED Lighting

The worldwide transition from incandescent bulbs to Light-Emitting Diodes (LEDs) for energy conservation is driving robust demand for HPA. HPA serves as the crucial raw material for producing synthetic sapphire substrates on which LED chips are grown. The high purity of the material is directly linked to the final LED product's brightness, efficiency, and lifespan, making 4N-grade HPA a fundamental requirement for the industry. The LED application segment has historically dominated the HPA market, accounting for a significant portion of total revenue. As governments and large corporations around the world implement policies to phase out less efficient lighting, the demand for HPA remains strong; for instance, more than 18 billion LED chips have been produced globally, relying on HPA-derived sapphire substrates. This ongoing infrastructural overhaul in lighting, particularly in rapidly urbanizing regions, ensures a consistent and large-scale market for high-quality HPA.

- Expansion of the Advanced Electronics and Semiconductor Industry

The relentless drive for smaller, faster, and more powerful electronic devices—including smartphones, servers, and components for 5G networks and Artificial Intelligence (AI)—requires an increasing volume of ultra-high-purity materials like HPA. HPA is used in various aspects of semiconductor manufacturing, from forming insulating dielectric layers to serving as a core component in advanced semiconductor packaging. The most stringent electronic applications demand the higher purity grades, such as 5N (99.999%) and 6N (99.9999%) HPA. The global semiconductor industry is growing substantially, nearing the one trillion-dollar mark in revenues, which significantly increases the baseline consumption of high-specification materials. For example, the HPA consumption in the semiconductor and electronics segment accounts for over 10,000 metric tons globally. Continuous innovation in this sector, aimed at miniaturization and enhanced performance, translates directly into a higher demand for HPA's unique properties, which support thermal management and structural integrity in sensitive electronic components.

Key Trends in the High Purity Alumina Market

- Shift to Sustainable and Lower-Cost Production Technologies

A major emerging trend is the industry’s pivot towards alternative, more environmentally friendly, and cost-efficient HPA production methods that move away from the traditional, energy-intensive aluminum-alkoxide hydrolysis route. Companies are increasingly investing in and commissioning facilities that utilize processes like Hydrochloric Acid (HCl) Leaching or solvent extraction from alternative feedstocks such as kaolin. These newer technologies can significantly reduce both the capital expenditure and the operating costs associated with achieving high purity. For example, some developers of new processes claim to achieve purity levels of 99.999% (5N) while reporting a substantial reduction in carbon emissions, sometimes by over 70%, compared to legacy methods. This trend is crucial for lowering the overall production cost of HPA, which is currently a high-priced specialty chemical, enabling its wider adoption in high-volume applications like battery components.

- Increasing Adoption of Ultra-High Purity Grades (5N and 6N)

There is a noticeable market pull towards HPA grades with purities of 5N and 6N (99.999% and 99.9999% respectively), driven by the most demanding and sophisticated applications. While 4N HPA is common in LEDs and standard battery coatings, the transition to next-generation technologies mandates an even higher level of material quality. For instance, in the semiconductor sector, the manufacture of advanced power electronics and certain epitaxy processes for Gallium Nitride (GaN) devices require 5N and 6N alumina to ensure component reliability and performance under extreme conditions. The demand for these ultra-pure grades is accelerating, with specific regions and advanced electronics sectors reporting a year-over-year increase in 5N product inquiries, sometimes as high as 33%. This trend signifies a qualitative evolution of the HPA market, where the performance ceiling is constantly being raised by the requirements of cutting-edge technology.

- Integration in Advanced Thermal Management Systems

HPA is increasingly being incorporated into new thermal management solutions, especially for high-power-density applications in EVs and advanced computing. Its excellent thermal conductivity and electrical insulation properties make it an ideal filler material for Thermal Interface Materials (TIMs), as well as a component in high-performance technical ceramics and heat sinks. The need for efficient heat dissipation is becoming paramount in electric vehicle power electronics, where components operate at high voltages and temperatures. The adoption of HPA in ceramic components for these systems is growing significantly, driven by the desire to maximize system efficiency and prolong component life. For example, new HPA-based materials are being used to manufacture advanced ceramic components that offer superior wear resistance and thermal control, essential for reliable operation in challenging industrial and automotive environments.

Leading Companies Operating in the High Purity Alumina Industry:

- Alcoa Corporation

- Altech Chemicals Limited

- Baikowski SAS

- Coorstek Inc. (Keystone Holdings LLC)

- Nippon Light Metal Holdings Company Ltd.

- Norsk Hydro ASA

- RusAL

- Sasol Limited

- Sumitomo Chemical Co. Ltd

- Zibo Honghe Chemical Co. Ltd.

High Purity Alumina Market Report Segmentation:

By Purity Level:

- 4N

- 5N

- 6N

The 4N segment, holding 42.0% of the 2024 high purity alumina market, dominates due to its cost-effective balance of high thermal stability, chemical resistance, and optical clarity, widely used in LED substrates, lithium-ion battery separators, and advanced electronics.

By Production Method:

- Hydrolysis of Aluminium Alkoxide

- Hydrochloric Acid Leaching

- Others

This method leads the 2024 HPA market for its energy-efficient production of high-purity (>99.99%) alumina with precise control over particle size and quality, ideal for LEDs, semiconductors, and lithium-ion batteries.

By Application:

- LED

- Semiconductor Substrate

- Phosphor

- Sapphire Glass

- Others

The LED segment, with 49.6% market share in 2024, dominates the HPA market due to HPA’s critical role in producing durable, thermally conductive sapphire substrates for energy-efficient LED lighting in automotive, electronics, and display technologies.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia-Pacific, with over 75.0% market share in 2024, leads the HPA market due to its robust consumer electronics, LED, and EV industries, supported by cost-effective raw materials, advanced manufacturing, and government initiatives like Australia’s AUD 400M HPA facility investment.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302