Market Overview:

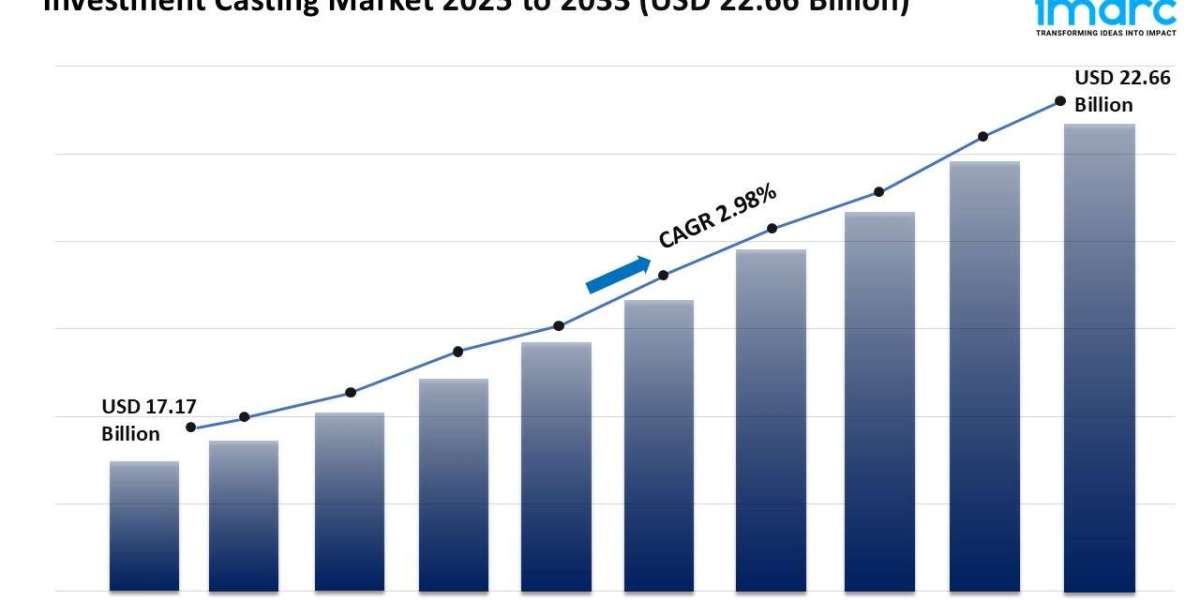

The investment casting market is experiencing rapid growth, driven by expanding demand from aerospace and automotive sectors, government incentives and modernization schemes, and technological advancements and industry consolidation. According to IMARC Group's latest research publication, "Investment Casting Market Size, Share, Trends and Forecast by Process Type, Material, Application, and Region, 2025-2033", the global investment casting market size was valued at USD 17.17 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 22.66 Billion by 2033, exhibiting a CAGR of 2.98% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/investment-casting-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Investment Casting Market

- Expanding Demand from Aerospace and Automotive Sectors

The investment casting industry is experiencing solid momentum thanks to surging demand for ultra-precise, complex metal parts in aerospace and automotive applications. For instance, North America holds a commanding 35% market share, propelled by heavy investments in aviation and a robust automotive manufacturing base. Lightweight, high-strength castings are critical for fuel efficiency and regulatory compliance, with companies like Precision Castparts reporting substantial double-digit growth in aerospace component revenues. As aircraft production and global vehicle electrification push manufacturers to deliver intricate, high-performance parts on tight timelines, investment casting’s versatility and accuracy keep it front and center for modern engineering challenges.

- Government Incentives and Modernization Schemes

Supportive government policies and incentive schemes across the globe are fueling industry expansion by de-risking capital investment and encouraging technology upgrades. In India, the “Atmanirbhar Gujarat” scheme offers up to 7% interest subsidies and generous net GST reimbursements for 10 years, making it attractive for large-scale casting projects. Simultaneously, the Credit Linked Capital Subsidy Scheme (CLCSS) provides up to 15% capital subsidies on plant and machinery purchases, accelerating tech adoption and capacity enhancement for both small and large units. These tailwinds have significantly boosted production and modernization, creating fertile ground for foundries to scale output and compete internationally.

- Technological Advancements and Industry Consolidation

With major players investing in next-gen automation, digital design, and advanced alloys, the investment casting landscape is transforming rapidly. For example, the recent merger of Texmo Precision Castings and Feinguss Blank, now operating as Texmo Blank, has created the only global investment casting specialist with production in the USA, Europe, and Asia. The combined operation employs over 1,750 skilled professionals and manages 1,000,000sq.ft. of manufacturing space. This consolidation means accelerated innovation: adoption of robotics, AI-powered defect detection, and digital simulation streamline processes and raise quality, making the industry more competitive and responsive to evolving customer needs.

Key Trends in the Investment Casting Market

- Push for Sustainability and Material Efficiency

Sustainability is quickly moving from buzzword to mandate in investment casting. Foundries are prioritizing recyclable materials, energy saving, and waste reduction to meet customer and regulatory expectations. Leading companies now invest in cleaner production methods, with modern manufacturing setups reducing scrap and recycling process waste. As environmental standards grow tougher, these practices not only reduce operating costs but also help cast parts compete for use in industries—from automotive to energy—where “green” credentials are vital. For example, top-tier foundries processing millions of high-precision parts annually are increasingly being certified for their low-impact and efficient operations.

- Integration of Automation and Digitalization

Digital advances are reshaping how castings are designed and manufactured. Robotics, automated shell-building, and real-time production monitoring are now mainstream, delivering tighter tolerances and more consistent quality across batches. Modern foundries employ digital twins and advanced simulation to avoid process bottlenecks and adapt production as customers tweak designs. Computer-aided manufacturing isn’t just about speed—it’s about agility, helping foundries reduce time-to-market and improve yields on even the most intricate components. Industries like aerospace, defense, and medical devices are at the forefront, relying on these improvements for both performance and regulatory compliance.

- Growth in Custom Healthcare and Energy Applications

Fresh demand is emerging as investment casting proves its worth in new sectors. The healthcare industry now leverages this process for custom implants, prosthetics, and surgical tools, benefiting from the ability to create intricate, patient-specific designs. In the energy sector, especially oil, gas, and renewables, the need for robust, wear-resistant cast components is soaring. Advanced foundries supply everything from high-precision turbine blades to critical infrastructure fittings. These applications are helping drive global market value, as local producers ramp up expertise and meet industry-specific requirements for quality and performance—keeping the market vibrant and responsive to evolving challenges.

We explore the factors propelling the investment casting market growth, including technological advancements, consumer behaviors, and regulatory changes.

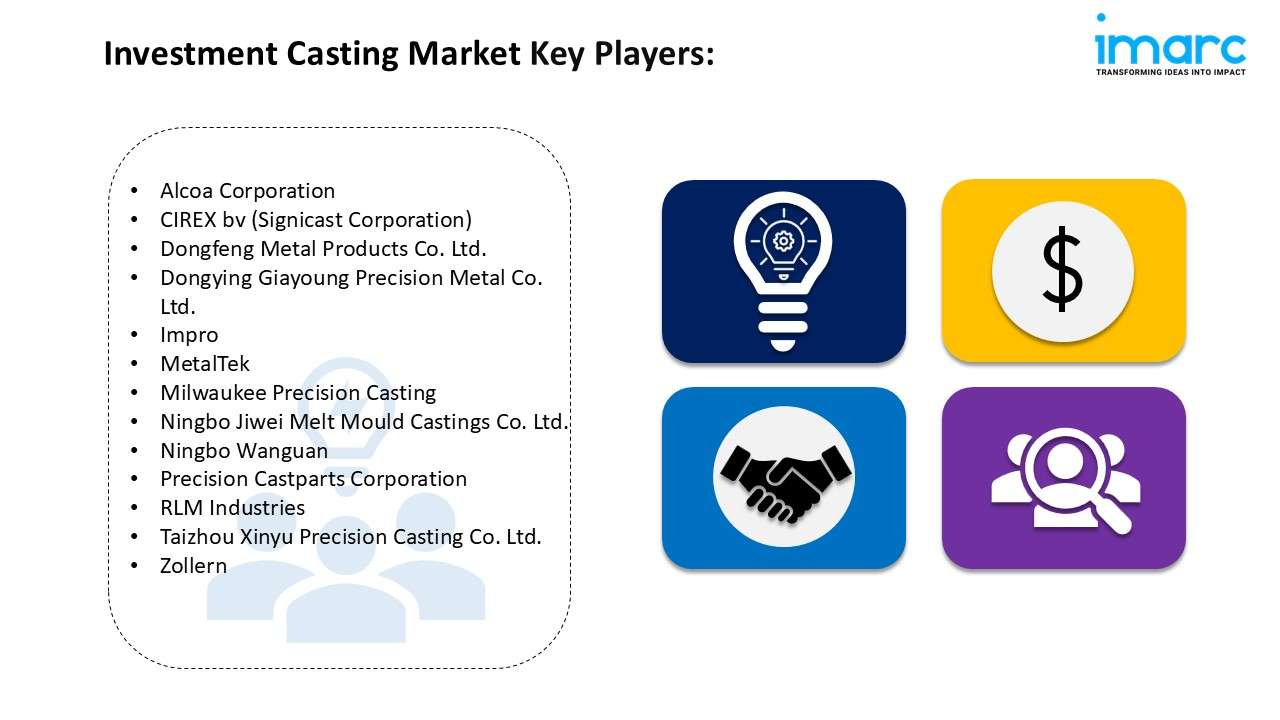

Leading Companies Operating in the Global Investment Casting Industry:

- Alcoa Corporation

- CIREX bv (Signicast Corporation)

- Dongfeng Metal Products Co. Ltd.

- Dongying Giayoung Precision Metal Co. Ltd.

- Impro

- MetalTek

- Milwaukee Precision Casting

- Ningbo Jiwei Melt Mould Castings Co. Ltd.

- Ningbo Wanguan

- Precision Castparts Corporation

- RLM Industries

- Taizhou Xinyu Precision Casting Co. Ltd.

- Zollern

Investment Casting Market Report Segmentation:

By Process Type:

- Sodium Silicate Process

- Tetraethyl Orthosilicate (Silica Sol Process)

Sodium silicate process dominates the investment casting market due to its advantages in mold stability, cost-efficiency, and environmental benefits, driving widespread adoption.

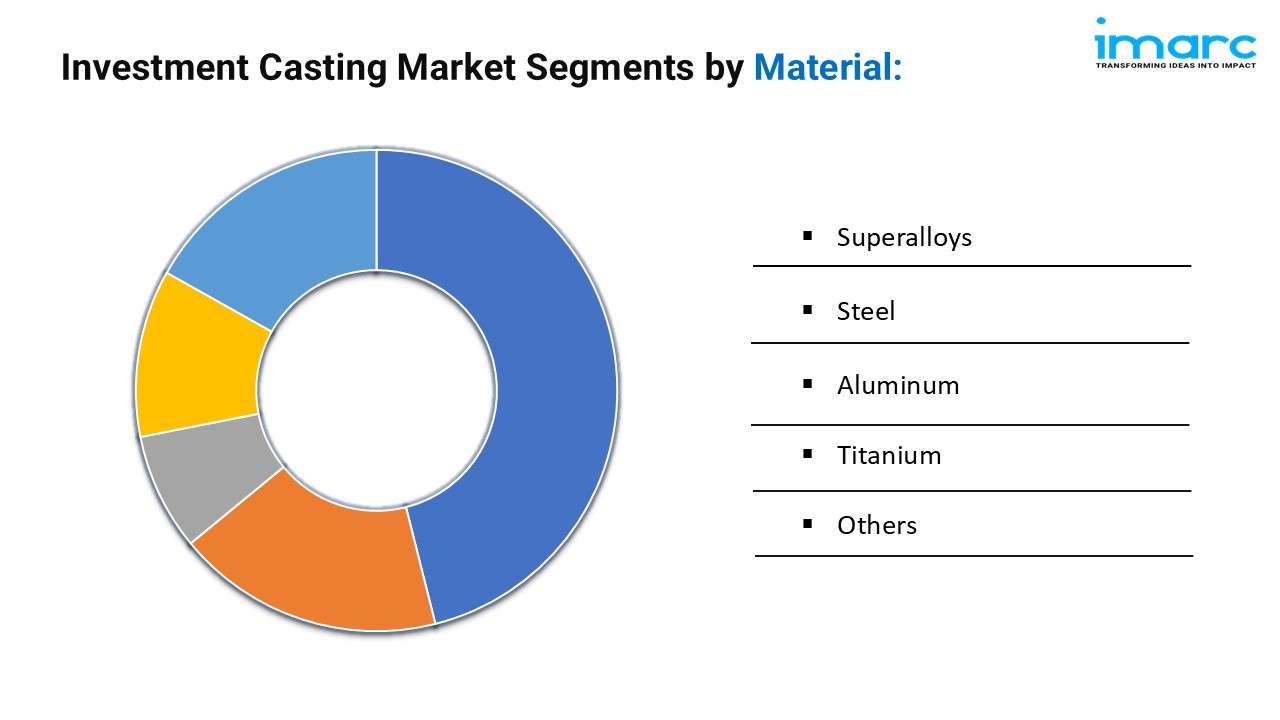

By Material:

- Superalloys

- Steel

- Aluminum

- Titanium

- Others

Steel holds the largest market share in investment casting, valued for its high strength, durability, and versatility in producing complex components across various industries.

By Application:

- Automotive

- Aerospace & Military

- Oil and Gas

- Energy

- Medical

- Others

Aerospace & military account for the largest market segmentation, as investment casting is essential for producing precise components that meet stringent performance standards in high-stress environments.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America leads the investment casting market, with significant contributions from the United States and Canada, supported by robust industry presence and demand across various sectors.

Research Methodology:

The report employs a comprehensive research methodology, combining primary and secondary data sources to validate findings. It includes market assessments, surveys, expert opinions, and data triangulation techniques to ensure accuracy and reliability.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302