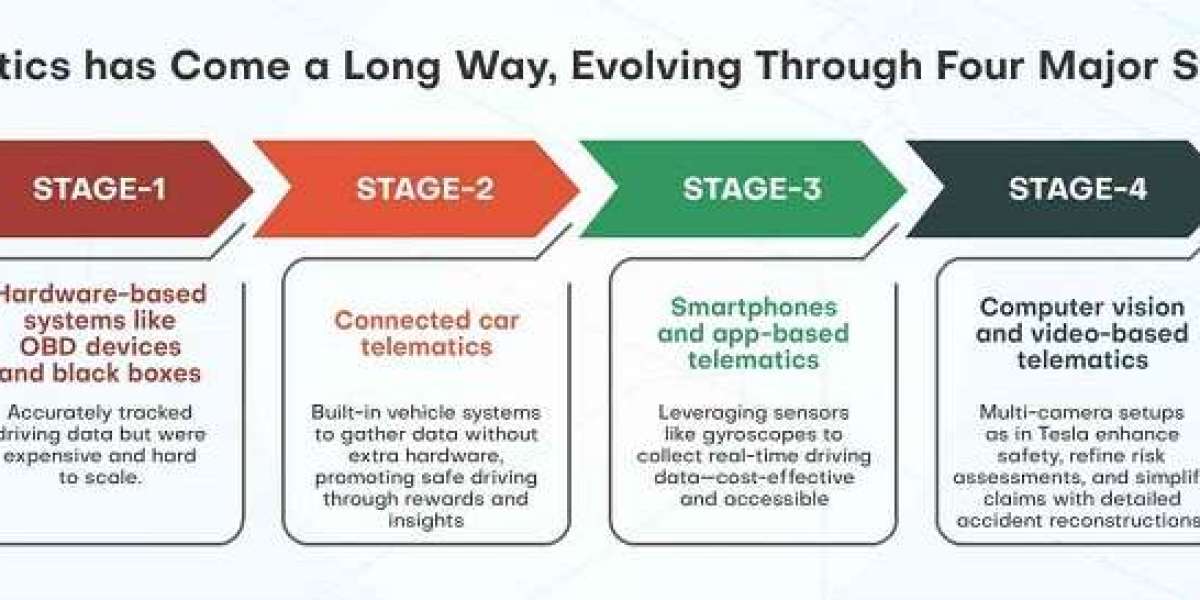

Smarter Data: From Metrics to Contextual Intelligence

The original telematics car insurance solutions were centered on collecting core driving data—things like speed, mileage, and braking behavior. Today, Telematics 2.0 goes much further. It doesn’t just track how someone drives; it analyzes where they’re driving, when, and under what conditions.

This next-gen approach blends driving behavior with contextual inputs like weather conditions, traffic density, and road quality. The result? A far more accurate picture of risk and better-informed policy decisions. This isn't about digitization for its own sake—it’s about adding real value for both insurers and policyholders.

Predictive Maintenance: A New Role for Insurers

Predictive maintenance has long been used in fleet operations, but personal insurance is just starting to unlock its benefits. With telematics-enabled diagnostics, insurers can shift from passive risk assessment to proactive safety partners—alerting drivers to issues before they become claims.

Take Munich Re, for example. Their solution offers plug-and-play apps or SDKs that allow insurers to integrate advanced telematics features into their platforms, providing flexibility and complete control over the user experience. These tools help insurers reduce risk and offer added value to their customers.

With AI-driven telematics car insurance, insurers can now forecast vehicle breakdowns and recommend preventative maintenance based on real-time data. State Farm and others are already using this model to improve customer outcomes and reduce loss ratios. Some insurers report up to 30% greater risk assessment accuracy and 20% fewer accidents thanks to predictive maintenance tech.

Behavior Change Through Gamification

UBI programs have traditionally rewarded safe drivers with discounts, but Telematics 2.0 introduces a deeper layer—behavioral influence. Insurers are now using gamification strategies to actively encourage safer driving habits. Features like points, badges, leaderboards, and rewards are being used to engage drivers and reduce risk.

Research from the University of Guelph highlights that gamification increases enrollment in telematics programs, particularly among younger demographics. Root Insurance has leveraged this concept successfully, tailoring premiums to driver behavior and seeing a notable drop in claims. Similarly, data from Cambridge Mobile Telematics shows a 40% reduction in accident risk when real-time feedback and incentives are applied.

Telematics as a Strategic Data Asset

Telematics data is also becoming a bridge for ecosystem collaboration. Insurers now have opportunities to partner with automakers, urban planners, and retail brands. For example, anonymized driving data can be shared with city planners to support smarter infrastructure, reduce congestion, and enhance road safety. Audi’s Traffic Light Information system is a great case—vehicles communicate with traffic systems to streamline traffic flow in urban areas.

Retail partnerships offer even more possibilities. By aligning driving behavior with consumer habits, insurers can offer personalized rewards and experiences. Progressive’s Snapshot program is one such model, using driver data to create lifestyle-based perks and deepen customer engagement.

AI-Powered Risk Analysis

With the massive amount of data generated by telematics car insurance, AI and machine learning have become essential tools for insurers. These technologies analyze patterns in driving behavior that traditional methods can’t detect, enabling more accurate real-time risk scoring and better fraud prevention.

AI also plays a growing role in speeding up claims handling, enhancing underwriting, and predicting high-risk behavior before an incident occurs—all contributing to a more proactive, customer-centric insurance model.

What’s Next for Telematics?

As the technology matures, a few major trends are expected to shape the future of insurance telematics:

Connected Vehicles + 5G: Faster networks will make real-time data exchange seamless, enabling instant policy updates and more responsive pricing models.

Embedded Insurance: Telematics will increasingly be built into vehicle sales and digital ecosystems, streamlining policy issuance and enhancing the user journey.

Sustainability Integration: Future systems will likely monitor carbon emissions and promote environmentally responsible driving, aligning insurance with global sustainability goals.

Final Thoughts

Telematics 2.0 is more than a technical upgrade—it’s a strategic pivot for insurers looking to stay ahead. By combining contextual intelligence, AI, and behavioral science, the industry is moving toward a more dynamic, personalized, and proactive approach to insurance. The real opportunity lies in how insurers leverage this transformation to build deeper relationships with customers, reduce risk, and create new value streams.