Market Overview:

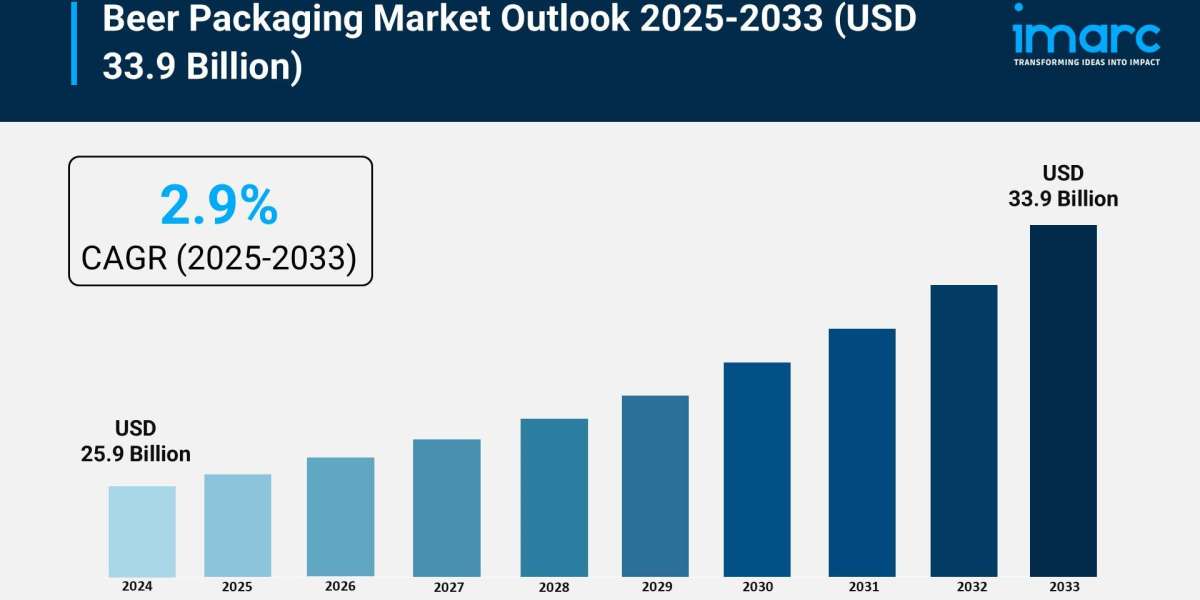

The beer packaging market is experiencing rapid growth, driven by sustainability mandates and consumer preference, the premiumization and craft beer boom, and expansion of e-commerce and direct-to-consumer channels. According to IMARC Group's latest research publication, "Beer Packaging Market Report by Material Type (Glass, Metal, Polyethylene Terephthalate (PET)), Packaging Type (Can, Bottle, Keg, and Others), Form (6-Pack, 4-Pack, 12-Pack), and Region 2025-2033", The global beer packaging market size reached USD 25.9 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 33.9 Billion by 2033, exhibiting a growth rate (CAGR) of 2.9% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/beer-packaging-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Beer Packaging Market

- Sustainability Mandates and Consumer Preference

The significant push for environmentally responsible packaging is a primary growth engine, directly influencing material choice across the beer industry. Driven by growing consumer awareness—where over three-quarters of global consumers report altering their purchasing habits based on environmental impact—breweries are aggressively adopting highly recyclable materials. This trend has fueled a resurgence in the use of aluminum and glass, as seen in the increasing market share of metal cans due to their high recycling rates and lightness for transport. Government initiatives like Extended Producer Responsibility (EPR) programs in numerous regions, such as the new laws passed in several US states, place the financial and physical responsibility for end-of-life management on producers. This encourages investment in circular packaging models, driving innovation in lightweight glass and bottles made with post-consumer recycled content, ensuring that sustainability is an economic and regulatory necessity.

- The Premiumization and Craft Beer Boom

The rising global consumption of specialty, premium, and craft beers is intensely driving demand for differentiated and high-quality packaging. Craft breweries, known for their unique branding and experimentation, rely on packaging to create a powerful shelf presence and convey an artisanal image. This has led to an increased use of custom bottle shapes, sophisticated finishes, and high-end labeling techniques, such as textured labels and embossing, to justify the higher price point of these products. Major packaging companies are capitalizing on this by offering advanced printing capabilities and smaller-volume production runs to cater to niche brands. The focus on aesthetics and product storytelling elevates the role of packaging from a mere container to a crucial brand identity tool, fostering innovation beyond standard, mass-market formats.

- Expansion of E-commerce and Direct-to-Consumer Channels

The rapid expansion of online retail and direct-to-consumer (D2C) beer delivery services is creating new demands for specialized packaging solutions that prioritize durability, security, and presentation during transit. As more consumers purchase beer for home consumption, packaging must be lightweight and robust enough to prevent breakage and damage in the complex shipping supply chain. This shift has particularly boosted the popularity of aluminum cans, which offer excellent protection against light, oxygen, and physical impact, alongside being stackable and convenient for logistics. Companies are also investing in tailored secondary packaging, such as protective cardboard bottle carriers and eco-friendly void fill, to ensure a premium unboxing experience. The need for shipping-safe, tamper-evident solutions is fundamentally reshaping the design requirements for beer containers.

Key Trends in the Beer Packaging Market

- Digital and Interactive Labeling

A key emerging trend is the integration of digital technologies directly into beer packaging to enhance consumer engagement and transparency. Breweries are increasingly incorporating Quick Response (QR) codes and Near-Field Communication (NFC) tags onto labels. For example, a consumer can scan a code to instantly access a specific beer's origin story, precise ingredient details, food pairing suggestions, or batch-specific production data, thereby building greater brand trust and offering a deeper consumer experience. This not only provides enhanced traceability, which aligns with consumer demand for authenticity, but also allows brands to dynamically update content without changing the physical label. This shift transforms static packaging into an interactive media channel, enabling personalized marketing and post-purchase follow-up with the drinker.

- The Rise of Smaller, Diverse Multi-Packs

The market is witnessing a trend toward diversified, smaller multi-packs that cater to consumer desire for variety, portion control, and convenience for at-home consumption. This trend moves away from single-format bulk packaging toward "variety packs" that group different beer styles or seasonal offerings into a single purchase. Packaging manufacturers are responding with innovative secondary packaging designs, such as cardboard carriers that securely house a mix of four or six cans/bottles, often featuring handles for easy portability. These packs are designed for immediate shelf appeal and allow craft breweries to introduce consumers to their range without requiring a large purchase commitment. This focus on format flexibility reflects changing social habits, where consumers prioritize sampling and a diverse selection of premium products.

- Alternative and Lightweight Material Innovation

Packaging innovation is focusing heavily on developing and commercializing new, non-traditional materials to reduce weight and environmental footprint. One compelling example is the ongoing development of fiber-based bottles, such as prototypes made from wood fiber that are designed to be bio-based and fully recyclable. This allows for a significant reduction in the reliance on virgin glass or metal, particularly in large-scale brewing operations. Furthermore, the practice of "lightweighting" traditional containers—reducing the material used in each glass bottle or aluminum can without compromising structural integrity—is a widespread strategy. This results in lower transportation emissions and material costs, demonstrating a material shift that balances robust product protection with aggressive sustainability targets.

Leading Companies Operating in the Global Beer Packaging Industry:

- Amcor plc

- Ardagh Group S.A.

- Ball Corporation

- Berlin Packaging

- Carlsberg A/S

- Crown Holdings Inc.

- Nampak Ltd.

- O-I Glass Inc.

- Plastipak Holdings Inc.

- Smurfit Kappa Group plc

- Verallia

- WestRock Company

Beer Packaging Market Report Segmentation:

By Material Type:

- Glass

- Metal

- Polyethylene Terephthalate (PET)

Glass leads the beer packaging market, holding the majority share due to its ability to preserve beer quality and its high recyclability.

By Packaging Type:

- Can

- Bottle

- Keg

- Others

Cans account for the majority of the market share owing to their lightweight, portable, and easily recyclable nature, appealing to consumer preferences for convenience and sustainability.

By Form:

- 6-Pack

- 4-Pack

- 12-Pack

6-Pack exhibits a clear dominance in the market on account of its popularity as a standard packaging format for retail sales, offering convenience, affordability, and ease of handling for both consumers and retailers.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position in the beer packaging market, driven by a strong beer consumption culture, a large number of breweries, and high levels of disposable income.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302